Cash is still a popular way to pay for services and goods, and can sometimes…

Car Buying Tips and Tricks: Beat the Dealer

How to Outsmart the Car Dealer

Selling cars is a business and with any business they want to make money. Dealerships want to make money and the sales people want to make commission. In car sales, money is made on the purchase of a vehicle, on the financing of said vehicle and all of the add-ons. Today with low car inventories, dealers aren’t negotiating much on car prices but there is room to save on financing and add-ons.

Here are some tips to help you keep more money in your pocket and beat the dealer.

Before heading out, check the dealership website or call/email

Instead of running around town stopping at every dealership, check their website first. If there is a car you are interested in, call or email the dealer. If you have a specific car in mind, call or email the dealership and get them to do some of the leg work for you. They can let you know of any cars that haven’t made it to the website yet or can let you know of any ‘just came in’ cars.

Find out what is in stock and the out-the-door price. And if you can get the price in writing with the sales manager’s signature, even better!

Cars.com is a great hub for new and used cars. MCU also offers AutoSmarts, showcasing new and used cars and you can get pre-approved all in one stop.

Decide on a trade-in or private sale

If you have a car to trade-in, check what the car is worth yourself. In today’s market with used car prices sometimes higher than new car prices, by selling the car yourself, you can get a lot more for a used car than the dealer might give you. From experience, dealers can offer you up to $7000 less for a car than you could get by selling it yourself.

If your car is paid off and you are selling it for the same or less than you purchased it for, you don’t have to pay taxes on the sale in Wisconsin. Just let the DMV know of the sale and you can fill out a Bill of Sale for your own personal records.

If you choose to trade-in your car, you will likely get more for it by taking it to the same brand dealership, a Ford Focus to a Ford dealer and Honda Civic to a Honda dealer. Dealers will often sell off-branded cars to another dealer who will then resell the car to the public. Same with very old cars, dealers will often sell them to independent car dealers or at auto auctions.

Remember each person along the way wants a cut from the deal, so it’s best to cut out the middlemen as much as possible.

Dealers love trade-ins. They can often make more money on a used car sale versus a new car one. If your car has less than 80,000 miles and is less than 6 years old, dealers will refurbish it and sell it for 15% – 20% more than you sold it for. If your car is less than 3 or 4 years old, dealers might be able to sell it as a pre-certified used car which adds $1000 – $1500 on top of the already 15-20%.

Don’t try to haggle

Unless you yourself are a car salesperson or salesperson, it’s going to be hard to beat the dealer at their own game. Plus, today’s market for new cars is a dealers market. There is more demand than supply so haggling will just frustrate you and drag the process out even further. Instead, force dealers to compete against each other.

Watch out for “fun” advertisements

If you received a mailer with the key to your dream car and a plastic key attached or a scratch-off and win section. Beware! These dealers pray on the desperate. They often offer low payments but drag out the terms so the value of the car will be less than you actually owe on it.

Speaking of payments…don’t

It’s good to be prepared. Know how much you can afford before going to the dealer. You can use a loan calculator, check with your credit union loan department to get pre-approved, or do your own calculations. Just know your limits. And don’t tell those limits to the dealer. Evade, evade, evade, because they will ask. And often, they won’t be able to give you that monthly payment you want… Not after they sell you all the add-ons.

Take off the Add-ons

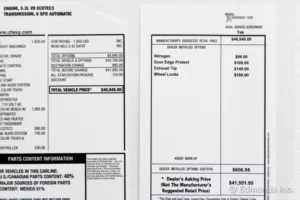

With new and used cars alike, dealers try to pile on the add-ons and accessories. They are likely to say that if you fold the cost into your loan, it will only add a few dollars to your monthly payment. But those add-ons can quickly jump from the hundreds to the thousands of dollars added to the sticker price. Some are dealer add-ons that they will try to slip past and others they will simply try to sell you. This is more commission and profit for the dealer/dealership. Assume the dealer adds a 50% mark-up to all add-ons.

Here is the low-down on some common add-ons:

- Fabric Protection – $195 for what a $9 bottle of Scotch Guard can do.

- Window Tints/UV Protection – odds are they have a third party do it and you could do the same at a fraction of the cost

- Door Edge Protector for $169 what you can do yourself with a kit from Amazon for $10

- Paint Protection for $495, when contacting the service department it’s basically a waxing

- Paint Sealants, car manufacturers choose paint to withstand the elements, which also often have anti-rust properties. Wash your car regularly and the paint will last, no pricey sealants necessary.

- Wheel Locks – pay $17 at AutoZone for four locks, one for each wheel instead of $189 at the dealer.

- Nitrogen in tires – Yes, nitrogen may have you filling your tires less often, however you can only fill your tires with nitrogen or the benefits of nitrogen disappear. So every time you do want to fill your tires, you have to pay a premium price instead of going to Kwik Trip for free. Plus air is free.

Beware of extended warranties, GAP Insurance and Vehicle Service Contract (VSC) coverage

Dealers earn a big profit from selling extended warranties, GAP insurance and VSC coverage. If you are in the market for these, it’s often better to negotiate this yourself with a third party or wherever you are getting pre-approved for your loan. MCU offers extended warranties through Vision who works with AllState Insurance and GAP insurance.

Know what you can afford

This cannot be stated enough. It’s all too easy to get caught up in the moment. You are finally getting your dream car and you’ve been at the dealership for hours already. You are excited and antsy that you start agreeing to $20 a month here and $15 dollars extra a month there and before you know it you have a huge monthly payment that you can barely afford.

Do your research ahead of time. Go to the dealer knowing how much you want to spend total and how much a month you can afford. Knowing those two numbers can save you time, money and a great big headache down the road.

Related Posts